Starting your home buying journey can seem daunting. But, with the right help, first-time buyers can tackle it with ease. Oak Real Estate offers a detailed Homeownership Guide to make each step clear.

The home buying process needs careful planning and smart choices. It includes checking your finances and learning about mortgages. Buyers need a clear path to owning a home.

Buying a home is a big financial step. Our team at Oak Real Estate is here to guide you through every important phase. We aim for a smooth and successful home buying experience.

Key Takeaways

- Know your financial situation before looking for homes

- Build a strong credit score for better mortgage rates

- Look into different loan options and lenders

- Plan for costs beyond the mortgage, like maintenance

- Work with experienced real estate agents

- Have all needed documents ready

- Be flexible during the home buying process

Understanding Financial Readiness for Home Purchase

Getting ready to buy a home means planning your finances well. You need to check your financial health first. Lenders look at several important things to see if you can buy a home.

Assessing Your Credit Score

Your credit score is very important when buying a home. It helps lenders decide if you can get a loan and what interest rate you’ll pay. Here are some key points about credit scores:

- Conventional loans need a credit score of at least 620

- FHA loans can work with scores as low as 580, with a 3.5% down payment

- A lower credit score might mean higher interest rates

Calculating Debt-to-Income Ratio

The debt-to-income (DTI) ratio is another key factor. It shows if you can handle your mortgage payments.

| DTI Category | Percentage Range | Lender Perspective |

|---|---|---|

| Ideal DTI | 36% or lower | Excellent financial health |

| FHA Loan Maximum | Up to 50% | Potential loan approval |

| Conventional Loan Limit | 43% or lower | Standard mortgage qualification |

Evaluating Savings and Income

Being financially ready is more than just credit scores and debt ratios. Here are some tips for saving:

- Try to save at least 20% for a down payment

- Plan for closing costs, which are usually 3% of the home’s price

- Keep an emergency fund while saving for your home

“Financial readiness is the foundation of a successful home purchase.” – Real Estate Expert

By looking at your finances carefully, you’ll be ready for the real estate world. You’ll be confident in your steps toward owning a home.

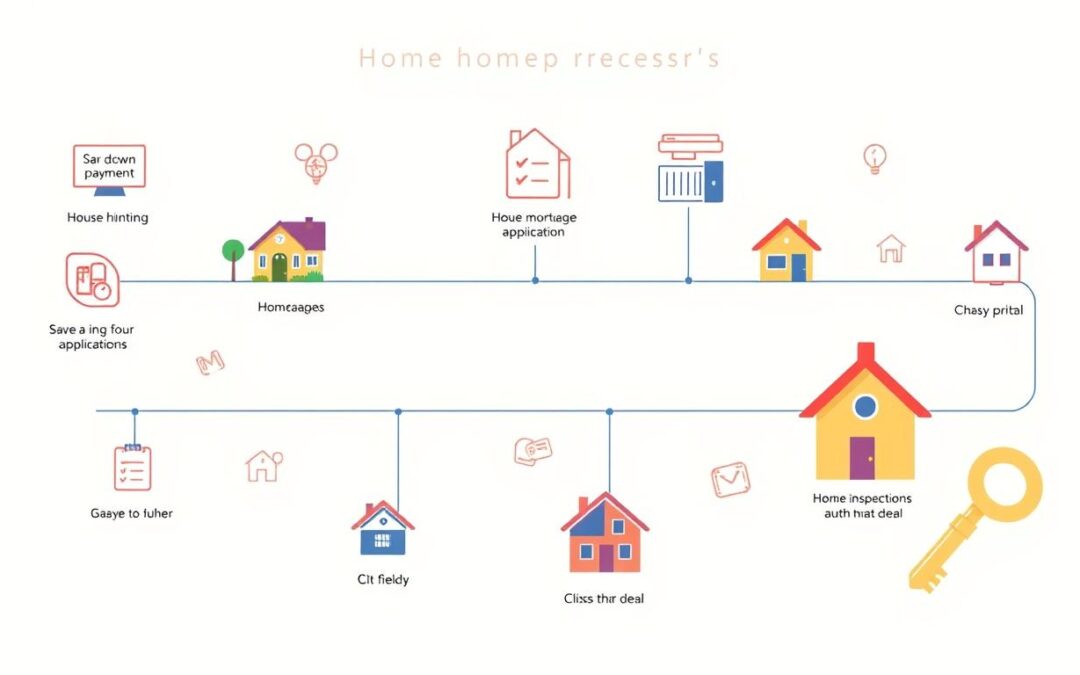

Step-by-Step Home Buying Process

Starting your home buying journey can seem daunting. But with a clear plan, it becomes an exciting adventure. Knowing each step helps you make smart choices and feel confident.

“Knowledge is power in real estate. The more you understand, the smoother your home buying experience will be.”

Here are the key steps in your home buying journey:

- Financial Preparation

- Check your credit score

- Calculate your debt-to-income ratio

- Save for a down payment

- Mortgage Pre-Approval

- Gather your financial documents

- Compare different lenders

- Get a pre-approval letter

- Property Search

- Know what you must have

- Research neighborhoods

- Work with a real estate agent

- Making an Offer

- Understand the market

- Find a good price

- Negotiate the terms

Did you know 85% of sellers only accept offers from pre-qualified buyers? This shows how vital financial prep is in your journey.

By following this structured path, you’ll turn a potentially stressful time into a well-planned journey. Remember, every step brings you closer to your dream home.

Down Payment Requirements and Options

For first-time homebuyers, down payments can be tough to handle. It’s key to know your mortgage options to make a wise choice. Let’s look at different down payment plans that can help you reach your dream of owning a home.

Traditional Down Payment Strategies

First-time homebuyers have a few traditional down payment options:

- Conventional loans usually need a 5% minimum down payment

- Some lenders offer loans with as little as 3% down

- Putting down 20% or more eliminates private mortgage insurance (PMI)

Government Assistance Programs

First-time homebuyers can get help from government mortgage programs:

- FHA loans offer down payments as low as 3.5%

- VA loans provide zero down payment options for qualified veterans

- State-specific programs offer extra down payment help

“A lower down payment doesn’t mean giving up on homeownership. It means finding the right financial plan for you.”

First-Time Buyer Incentives

There are many incentives to lower the cost of buying a home:

| Program | Down Payment Requirement | Credit Score Range |

|---|---|---|

| Rocket Mortgage | 1% for qualified buyers | 620-680 |

| New American Funding | 3.5% with state assistance | 580-620 |

| NBKC Loans | 3% conventional loans | 640-660 |

Your financial situation will guide the best down payment plan. Talking to a mortgage expert can help you find the right path to homeownership.

Exploring Mortgage Types and Financing

Understanding mortgage financing is key when buying a property. There are many mortgage types, each with its own benefits. They cater to different financial situations and needs.

The mortgage financing world offers several main options:

- Conventional Mortgages: Great for those with high credit scores (700+)

- FHA Loans: Perfect for first-time buyers with lower scores

- VA Loans: Only for military veterans and service members

- USDA Loans: For buyers in rural and suburban areas

Important factors to consider in mortgage financing include:

- Credit score needs

- Down payment amount

- Interest rates

- Loan term lengths

“Choosing the right mortgage is about matching your financial situation with the most suitable loan type.” – Real Estate Financing Expert

Fixed-rate and adjustable-rate mortgages differ in interest management. Fixed-rate mortgages last fifteen to thirty years, keeping payments steady. Adjustable-rate mortgages (ARMs) start with lower rates that change yearly, helping those expecting income boosts.

For unique needs, options like jumbo loans or interest-only mortgages exist. It’s vital to work with experts to navigate the complex property purchase steps.

Getting Pre-Approved for a Mortgage

First-time homebuyers face a tough mortgage landscape. A pre-approval is key, showing your buying power. It’s a big step in the homeownership journey, helping you stand out in the market.

Knowing the pre-approval process boosts your confidence. Lenders check your finances to see how much they can lend.

Required Documentation

Start by getting your financial documents ready. You’ll need:

- Proof of income (W-2 forms for the past two years)

- Recent pay stubs

- Bank statements

- Tax returns

- Credit history documentation

“A well-prepared document package can significantly improve your chances of mortgage pre-approval.” – Real Estate Finance Expert

Understanding Pre-Approval Terms

Pre-approval is more than a first step. Nearly 70% of real estate agents emphasize its importance over a simple pre-qualification. Your pre-approval letter will include:

- Maximum loan amount

- Potential interest rate

- Loan type

- Validity period (usually 60-90 days)

Shopping for Lenders

Comparing lenders is smart. Experts recommend approaching at least three different lenders to find the best rates. Look at:

- Interest rates

- Loan terms

- Fees and closing costs

- Customer service reputation

Tip: A credit score of 740 or above gets you the best rates. But, many lenders offer options for lower scores too.

Working with Oak Real Estate Professionals

Buying a home is a big step, and Oak Real Estate is here to help. Our Realtor Services are designed to make your home buying journey easier. Our team knows the ins and outs of real estate and is ready to support you every step of the way.

“Choosing the right real estate professional can make the difference between a stressful purchase and a smooth transition to homeownership.”

Our realtors have the skills you need to find your dream home:

- Personalized market analysis

- Strategic property identification

- Skilled negotiation techniques

- Comprehensive transaction support

At Oak, we know every buyer is different. We create strategies that fit your needs and budget.

Our Realtor Services go beyond just finding homes. We offer:

- Detailed market insights

- Property valuation expertise

- Negotiation representation

- Comprehensive transaction management

Ready to start your home buying journey? Contact our team. We’re here Monday through Friday, ready to make your real estate dreams come true.

| Contact Method | Details |

|---|---|

| Phone | (435) 640-7297 |

| Alternative Phone | (435) 879-9255 |

| Hours | 9:30am – 8:30pm |

Property Search and Home Evaluation

Finding the right home is a big step. It starts with knowing what makes a house perfect for you. This means looking at important details that turn a house into your dream home.

Location Considerations

Choosing the right location is key. Think about:

- How close it is to work

- The quality of local schools

- Access to shops and services

- How safe the area is

- Its growth and development

Property Types and Features

There are many types of homes for different lifestyles. Here are some options:

| Property Type | Best Suited For | Average Price Range |

|---|---|---|

| Single-Family Home | Growing families | $350,000 – $600,000 |

| Townhouse | Urban professionals | $250,000 – $450,000 |

| Condo | First-time buyers | $200,000 – $350,000 |

Market Analysis

Knowing the local market is important. As of May 2024, median sales prices in the Triangle region vary:

- Wake County: $503,000

- Johnston County: $368,500

“More than 50% of homebuyers find their realtor through personal recommendations” – National Association of Realtors®

Use online listings and visit homes in person. Also, work with real estate experts. They can give you detailed insights into the market.

Making a Competitive Offer

Making a competitive offer is key in the Buyer’s Journey. It requires smart thinking and knowing the market. In today’s fast-paced real estate world, buyers need to be creative to stand out.

“A well-crafted offer is your first negotiation tool in securing your dream home.” – Real Estate Professional Insight

Here are some strategies for making strong offers:

- Research recent sales in the area

- Know the current market

- Have a solid financial profile ready

- Be open to different closing dates

The market now needs smart offer strategies. Here are some interesting facts:

| Offer Metric | Current Market Statistics |

|---|---|

| Average Days on Market | 24 days |

| Homes Selling Above List Price | 30% |

| Average Offers per Property | 2.8 |

| Typical Earnest Money Deposit | 1-3% of purchase price |

In tough markets, smart buyers use escalation clauses and big earnest money deposits. Bidding a bit higher than the asking price can make your offer stronger. Cash offers or few contingencies can also give you an edge.

Getting help from a seasoned real estate agent can make your offer stand out. They know the market well and can guide you through tough negotiations. This increases your chances of a successful Real Estate Transaction.

Home Inspection and Appraisal Process

Buying a home involves checking its condition and value. The home inspection and appraisal are key steps in your journey. They give you important insights before you buy.

Knowing about these evaluations helps protect your investment. It ensures you make a smart choice. Let’s look at what home inspection and appraisal involve.

Understanding Inspection Reports

A home inspection usually costs $325 and takes two to three hours. Inspectors check many things:

- Structural integrity

- Electrical systems

- Plumbing infrastructure

- Roof and foundation conditions

- Potential safety hazards

Negotiating Repairs

Inspection reports can show important details that affect your decision. You might find:

- Structural damage needing big repairs

- Electrical system problems

- Plumbing or water damage

- Potential safety issues

“An informed buyer is a protected buyer” – Real Estate Expert

Appraisal Requirements

Home appraisals cost between $300 to $450. They assess the property’s market value. Appraisers look at:

- Comparable property sales

- Property condition

- Local market trends

- Home improvements and features

The appraisal process takes one to two weeks. The first visit is within 48 hours of the lender’s order.

Understanding Closing Costs and Fees

Buying a home means understanding closing costs. These costs are a big part of the home buying process. They can be 3% to 6% of the loan amount, which is a lot of money.

“Know your closing costs before you close the deal – knowledge is financial power.”

When it comes to Mortgage Financing, there are several costs to expect:

- Lender fees and origination charges

- Title insurance and search expenses

- Property appraisal costs

- Government recording charges

- Prepaid property taxes and insurance

Here’s a simple list of typical closing costs:

| Expense Category | Average Cost |

|---|---|

| Appraisal Fee | $300 – $600 |

| Credit Report Fee | $15 – $30 |

| Pest Inspection | $100 |

| Lead-Based Paint Inspection | $336 |

| Origination Fees | Approximately 1% of Loan Amount |

Pro Tip: Some closing costs can be negotiated or potentially reduced with careful planning and understanding of the real estate market.

For a $200,000 home, you might spend $6,000 to $12,000 on closing costs. These costs can vary a lot, depending on where you live. Places like Washington D.C. have much higher costs than states like Missouri.

Final Walk-Through and Property Transfer

The final walk-through is a key step in your Home Acquisition Roadmap. It lets buyers check the property’s condition before the Closing Process. This usually happens within 24 hours of closing.

This check ensures everything is as agreed upon. It’s a chance to catch any last-minute issues.

“A thorough final walk-through can save you from unexpected surprises after moving into your new home.” – Real Estate Expert

During the final walk-through, buyers should look at a few important things:

- Verifying agreed-upon repairs are completed

- Checking that property condition matches the purchase agreement

- Testing all electrical outlets and systems

- Examining for any new damages

About 30% of buyers find issues during this walk-through. The time it takes can vary, depending on the property’s size and details.

Oak Real Estate suggests bringing important tools for the final inspection:

- Phone charger to test electrical outlets

- Measuring tape for verifying room dimensions

- Flashlight for examining dark areas

- Copy of the inspection report

If big problems are found, buyers have choices. They can ask for repairs, closing credits, or even delay the closing. Your real estate agent can help find the best solution for a smooth transfer.

Remember: The final walk-through is your last chance to fix any property concerns before becoming a homeowner.

Legal Aspects of Home Buying

Understanding the legal side of buying a home is key. It helps protect your investment and makes the process smoother. Knowing the legal steps is essential for a successful home purchase.

Buying a home involves many legal steps. These steps protect both the buyer and the seller. Getting help from a professional is important. They can help you understand complex documents and protect your rights.

Contract Review: Protecting Your Interests

Reviewing contracts is a critical step in buying a home. Buyers need to carefully look at purchase agreements. They should focus on important parts like:

- Contingency clauses

- Financial obligations

- Property condition stipulations

- Potential exit strategies

Title Search and Insurance Essentials

Doing a title search is important. It helps find any issues with the property’s ownership. About 40% of buyers don’t check documents well enough. This can increase the risk of problems during the transaction.

| Title Insurance Component | Average Cost | Coverage |

|---|---|---|

| Standard Policy | $500-$1,500 | Basic Property Rights Protection |

| Extended Policy | $1,500-$3,500 | Comprehensive Legal Defense |

Property Deed Transfer Process

The deed transfer is when you officially own the property. Careful documentation ensures legal recognition of your property rights. Most deals have a final walkthrough to check the property’s condition.

“Knowledge of legal procedures transforms a complex transaction into a confident investment.” – Real Estate Expert

Understanding these legal aspects helps buyers feel more confident and protected. It makes the home buying process smoother.

Conclusion

The home buying process is a big journey. It needs careful planning and expert help. Oak Real Estate’s Realtor Services guide you through it all. They help you make smart choices for your future.

Buying a home is more than picking a place. It’s about getting your finances ready. This includes checking your credit score and looking at mortgage options. Experts say to spend no more than 25% of your income on a home.

Success in real estate depends on many things. These include where the home is, how much people want it, and if you can afford it. With this guide and Realtor Services, you’ll know how to buy a home wisely.

Buying a home is a big deal. It’s not just about money. It’s about finding stability, growing your investment, and feeling fulfilled. Oak Real Estate is here to help you every step of the way.